Table des matières

Introduction

Asset allocation, why? In other articles, we explored the importance of real estate with Bricks, liquidity through Trade Republic (multi-banking), my favorite ETF tracking the MSCI World index (passive equity fund), commodities, bonds, and why frugalism leads to sound asset allocation. Today, we are going to examine why the golden rule of long-term finance is asset allocation.

It directly influences your portfolio’s performance, enables better risk management, and adapts to your goals, whether you are young or older. Moreover, all finance professionals agree on its crucial importance

What is asset allocation ?

Let’s start by breaking down assets: I’ll briefly cover monetary assets to focus on the essential distinction between financial assets and physical assets, which form the basis of asset allocation.

Physical assets: these are tangible, such as your primary residence, gold bars, or jewelry, for example.

Financial assets: these are equally clear, such as cash, stocks, bonds, mutual funds, cryptocurrencies, or bank deposits.

Asset allocation is the subtle art of distributing your wealth among these different asset categories. The key lies in your choices, as they will shape your long-term financial performance. Asset allocation is also about finding the delicate balance between expected returns and the level of risk you are willing to take. Think about it: the distribution of your wealth deserves careful consideration

Example of asset allocation :

| Stocks | 60% |

| Bonds | 20% |

| Savings accounts | 15% |

| Gold | 4% |

| Cryptomonaie | 1% |

| Total | 100% |

Why is asset allocation the #1 criterion ?

According to research, it is estimated that 90% of a portfolio’s long-term performance is linked to asset allocation rather than to security selection or market timing

A landmark study by Brinson in the 1980s revealed that asset allocation (the distribution between stocks, bonds, cash, and other assets) determines about 90% of the variability of a portfolio’s long-term returns—far more than stock selection or market timing.

This is therefore the key to maximizing your performance while controlling risk. Through the power of diversification, a strategic allocation across asset classes that move differently reduces volatility and improves your results.

For example, a balanced portfolio with 60% stocks and 40% bonds can absorb market shocks while aiming for growth.

In short, a well-thought-out asset allocation is your best asset for investment success.

HOW TO BUILD YOUR ASSET ALLOCATION ?

Building your asset allocation relies on three key steps: assessing your profile (goals, investment horizon, risk tolerance), analyzing the economic context, and diversifying strategically

- Assess your profile: Determine your goals (retirement, real estate purchase) and your time horizon (short, medium, or long term).

For example, a young investor may accept more risk, while a retiree will prefer safety

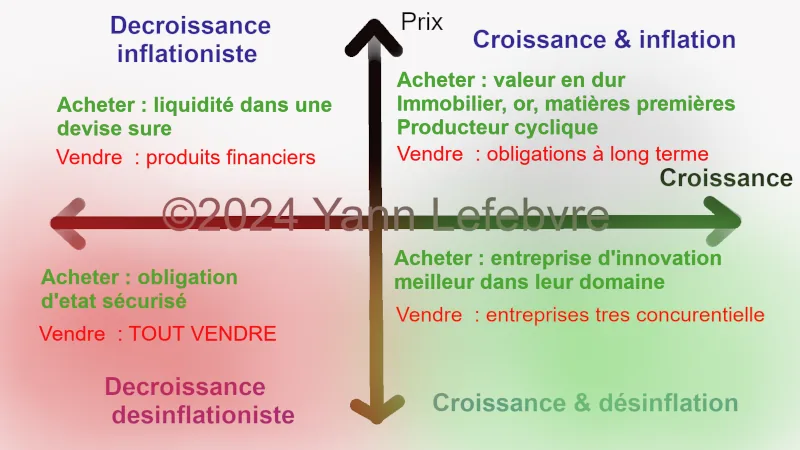

- Analyze the economic context: Use tools like the on-screen chart to identify economic phases (growth/inflation, contraction/disinflation, etc.)

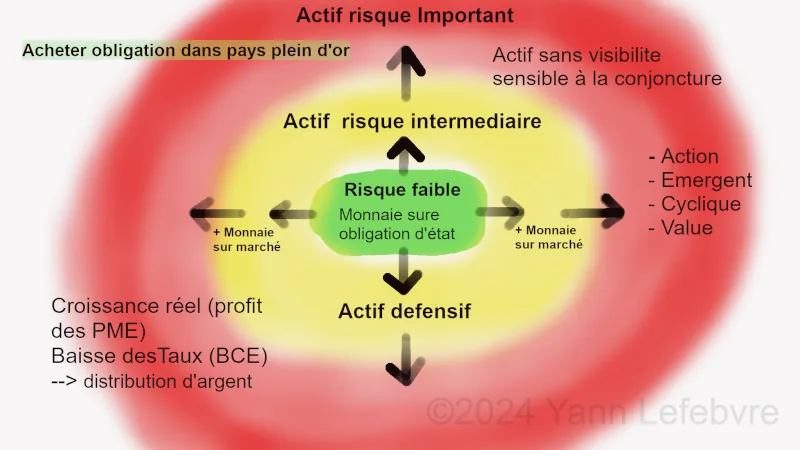

- Diversify strategically: Allocate your wealth according to the following chart, which classifies assets by risk level

In 2025, if the economy is in a growth-with-inflation phase (top-right framework), favor assets like real estate or commodities. In the event of an economic slowdown with less rapid price increases…

Example : For a balanced profile :

- Defensive assets (low risk): Safe-haven currencies + government bonds (e.g., 30%).

- Intermediate assets (moderate risk): Stocks or SMEs (e.g., 40%).

- High-risk assets (high risk): Emerging or cyclical stocks (e.g., 20%).

- No visibility: Set aside a small portion (e.g., 10%) for assets like cryptocurrencies, if your risk tolerance allows it.

My personal experiences and mistakes to avoid

When I first started investing in the stock market, I was unaware of this variable. A bad experience had convinced me that acquiring a roof over my head quickly was essential. As the saying goes: ‘Better a small home of your own than a grand one belonging to others.’

I learned lessons from my mistakes over time. After twenty years of financial disappointments in France and policies detrimental to the country, I decided to turn away from local investments, except for fully globalized companies that generate their revenue abroad

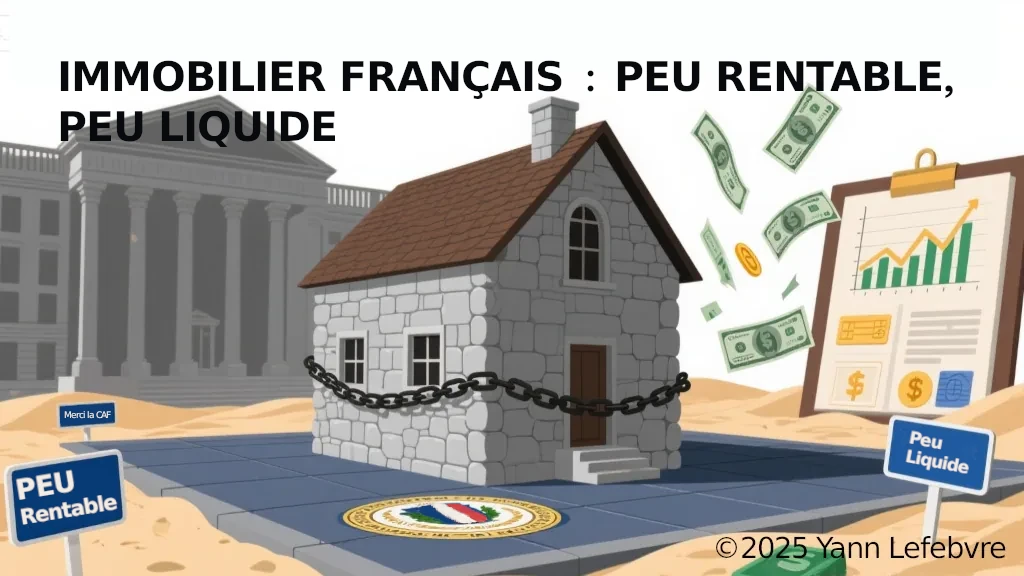

My disillusionment includes French real estate. Although I own my primary residence, I strongly advise against rental property investment in France today. Around me, feedback on rental real estate has been limited to failures, with disappointing returns.

SUMMARY: On one hand, the CAF (the state) gives you money, and on the other, the state taxes you! (TAXATION AND STUPID LAWS)

Real estate, often constrained by state and human factors, lacks the liquidity offered by my other physical or financial assets. For me, it is a distinct asset category, far less appealing, except to add a touch of diversity to my portfolio.

Be careful not to fall in love with your holdings! Whether it’s a favorite stock or a property, this attachment can lead to overinvesting. To remedy this, set clear limits: cap each asset at 10-20% of your portfolio and reassess regularly

What is the view of professionals on the global economy in 2025 ?

You’re wondering where the global economy is heading? Experts tell us we’re at a fascinating moment, with growth slowing slightly, prices remaining high, climate challenges, the lingering effects of the pandemic, and tensions between countries.

In 2025, they advise caution and adaptability.

For example, some, like those at J.P. Morgan, suggest betting on U.S. and Japanese stocks, which remain solid, and on investments like bonds for good returns.

Others, at BlackRock, believe that investing in projects like renewable energy or infrastructure can provide protection against rising prices.

In short, they say: diversify your savings with a variety of choices to be ready for anything!

Example of a professional opinion: Views on Asset Allocation – Q4 2024 from JPMORGAN ASSET MANAGEMENT

Anticipating the future: my vision of asset allocation

Since COVID, my vision has been clear-eyed but not pessimistic, because France is only a fragment of the global economy. If the West risks decline, other regions are booming economically and asserting themselves. A perspective rich in opportunities!

To illustrate asset allocation: in times of crisis, go all-in on a safe-haven currency and Asian bonds! Conversely, if growth takes off, invest heavily in stocks with strong competitive advantages (see the allocation chart based on the economy)!

Between these extremes, many opportunities open up with bonds, gold, or real estate! In short: if your bonds offer a better yield with dividends than your stocks, favor them! In difficult economic times, bonds form a shield against stock market turbulence

Bank savings accounts and euro-denominated life insurance contracts are, in reality, French government bonds! However, since my trust leans more toward the Romanian state than the French one, you can imagine the direction of my allocation in this category…

Conclusion : synthesis between your views and professional insights

My experiences have guided me toward a thoughtful geographical allocation: investing in countries where entrepreneurship thrives, like the United States, seems promising to me.

By combining my vision with the views of independent financial experts, I have learned to diversify wisely. Your asset allocation will depend on your vision of the future and major global political decisions.

To stay informed, explore a variety of sources beyond traditional media (this has opened my eyes)! Ready to refine your strategy

An example of asset allocation that reflects who I am

| Stocks | Stocks | France (C.A à l’internationale) | 26% |

| Stocks | Stocks | Foreign (Chine) | 23% |

| ETF-ETC (passif) | ETF-ETC (passif) | Foreign (United States, emerging and paper gold) | 20% |

| Gold | physical | Suisse | 10% |

| Real estate | Contractual & fixed income | Bricks | 10% |

| Cash | Multi-banking | 10% | |

| Bonds | Foreign state | 1% |

Examples of asset allocation in video

IMPORTANT DISCLAIMER

I am not a financial advisor! What I share are my personal reflections, successfully applied, but not investment advice. My ideas mix summaries and personal opinions, and they are solely my own. Take them as food for thought, not as instructions. Educate yourself, explore multiple sources, and tailor your choices to your profile: age, budget, risk tolerance, personal situation. No buy or sell recommendations are made here. You alone are responsible for your financial decisions. Consult an expert!