Table des matières

Introduction to Financial Bonds

Financial bonds are the last asset class I haven’t yet explored on my site. This is mainly because I hold very few of them, favoring gold and stocks in my asset allocation. The economic situation in Western societies reinforces my reluctance to lend over the long term. Fortunately, there are various types of bonds. After stocks, commodities, and real estate, here is my take on bonds, with a focus on those I actually own.

What are financial bonds ?

Unlike stocks, which represent a share of ownership in a company, bonds are financial instruments corresponding to debt securities acquired through a management company. In plain terms, buying a bond means lending money to a government or a company in exchange for an annual interest rate and a promise of repayment at maturity. Example: I lend €1,000 to the French government at 2% per year for one year. This example is to be avoided, as I would never lend to the French government, even at 3%, for political, economic, and moral reasons.

Basic vocabulary to understand financial bonds

To fully understand bonds, you need to know a few key terms, and I’m going to explain them simply !

- First, the issuer: this is the entity to whom you lend your money, such as a company (e.g., Alphabet) or a state (e.g., Romania).

- Next, the face value (or par value): this is the amount you lend, say €1,000.

- Then, the interest rate, or coupon: this is what you earn in return, for example 2% per year, or €20. These interest payments can be made monthly, quarterly, or annually, depending on the bond. It’s a bit like the dividends that companies pay you annually, semi-annually, or monthly.

- The maturity: this is the duration of your loan, for example 5 years, after which you get your €1,000 back. Simple, right ?

And one final point: risk. If you lend to a fragile company, there’s a chance it won’t be able to pay you back. That’s why it’s crucial to choose your issuer wisely !

Different types of bonds

There are all kinds of bonds out there !

First, you have those issued by governments, such as German or U.S. Treasury bonds, often considered very safe. Then, there are corporate bonds, across various sectors: technology, energy, healthcare, and many others. You can choose based on the loan duration—from 1 to 30 years, for example—and the interest rate, which depends on the issuer’s creditworthiness. There are also more specific bonds, like green bonds, used to finance environmentally friendly projects. To invest, you go through a bank or a broker, so be sure to compare their offerings to find the best opportunities !

How to choose financial bonds ?

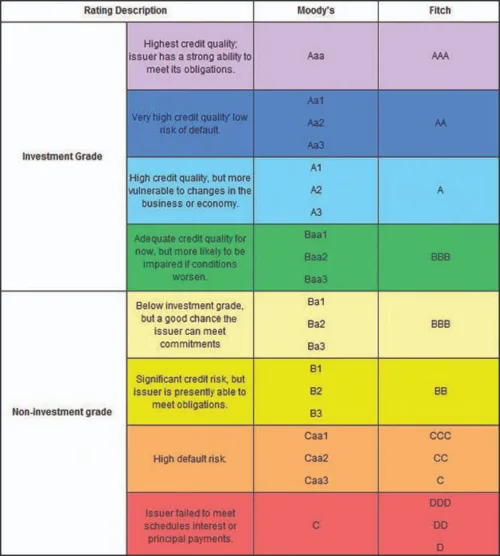

Unlike stocks, price is not the main criterion when choosing a bond. The key is to assess the quality of the issuer, the interest rate (coupon), and the maturity. Rating agencies such as Standard & Poor’s, Moody’s, and Fitch conduct in-depth evaluations of companies, states, or local authorities, and assign them a rating. As with a personal loan, a high-quality issuer gets a better rate but offers a lower coupon, with a stronger guarantee of repayment at maturity.

Bond evaluation grid :

- At issuance: a longer maturity increases risk, so the coupon is often higher (and vice versa).

- A weaker issuer implies greater risk, hence a higher coupon (and vice versa).

- Yield and bond price move in opposite directions: when one goes up, the other goes down. This matters little if you hold the bond until maturity.

- At issuance, the longer the maturity, the greater the risk, and the higher the bond’s coupon tends to be. And vice versa.

Bond ETFs do exist (see the article on the MSCI World ETF), but their fees seem high to me for a passive strategy like mine, which favors buying corporate or foreign government bonds and holding them until maturity. My goal is to diversify my wealth through asset allocation. I do not venture into complex mechanisms or active strategies, which I do not master.

Buying financial bonds

It’s simpler than you might think, and it can boost your portfolio diversification! Personally, I’m not a big fan of bonds or bond ETFs, but I’ll show you how to do it wisely.

Step 1: go through an intermediary. You can buy bonds through your bank TRADE REPUBLIC or an online broker like Degiro.

For example, you can lend directly to a government or a company via your banking app, or choose a basket of bonds through bond ETFs like the iShares Core EUR Corporate Bond, with fees of 0.2% per year, which bundles together hundreds of corporate bonds for easy diversification.

Step 2: choose your issuer carefully. Check their creditworthiness using ratings from agencies like Moody’s or Fitch – AAA is the top grade, but sometimes a slightly lower-rated issuer, like an undervalued company, can offer a better yield with reasonable risk.

Personally, I prefer to avoid certain issuers that are too risky, regardless of their rating, and favor bonds from foreign governments or solid companies, holding them until maturity.

Step 3: consider your goals. Are you looking for regular income or maximum safety? A 5-year or 20-year bond?

Step 4: watch the economic environment. If interest rates rise, bond values can fall, especially for ETFs.

Step 5: check liquidity. Make sure you can sell easily if needed, especially for ETFs, which trade like stocks.

Finally, diversify: don’t put everything into a single bond or a single ETF to limit risk.

For my passive strategy, I prefer to buy bonds directly to avoid ETF fees and keep things simple, but ETFs are perfect if you want a ready-made basket without overcomplicating things!

Concrete example of an interesting bond in 2023

For a concrete example of an interesting bond, let’s look at the Romanian government bond with ISIN XS2689949399. You lend €1,000 to the Romanian government, which pays you about 3.5% interest per year (€35), paid regularly, and returns your €1,000 in 10-15 years.

| Product name | Roumanie, République 5,5% 23/28 |

|---|---|

| Code ISIN | XS2689949399 |

| Link on DEGIRO | https://www.boerse-frankfurt.de/bond/xs2689949399-rumaenien-republik-5-5-23-28 |

| Issuer rating | Moody’s : Baa3 – S&P et Fitch : BBB- (Low default risk) |

| Issuer type | Government |

| Maturity date | 18 spet 2028 (4 ans) |

| COUPON | 5,5% |

| Coupon frequency | Annual |

Why it’s great for me? It’s a solid foreign government, with a BBB- rating that seems somewhat undervalued given Romania’s growth, and an attractive yield without ETF fees.

Watch out for political risks, but diversify and hold until maturity for a simple passive strategy. Check the details on your broker – it’s accessible to everyone!

Here’s a captivating video in French, with automatically translated subtitles on YouTube, that could reinforce or completely challenge my views on this fascinating country: Romania.

Economic information on Romania : https://datacommons.org/place/country/ROU?mprop=amount&popt=Debt&cpv=debtor,Government&hl=fr

IMPORTANT DISCLAIMER

I am not a financial advisor. I share thoughts that I personally apply and am happy to pass along. This is not investment advice. The views expressed are summarized and mixed with personal reflections that are solely my own. These are ideas to consider; it is essential to educate yourself and seek multiple sources of information to make informed decisions. No buy or sell recommendations are made. Each individual must invest according to their investor profile, risk tolerance, budget, age, personal and family situation, level of financial literacy, and investment horizon. Everyone is responsible for their own financial decisions.