Table des matières

Introduction

Do you dream of putting your money to work to generate passive income—even while you sleep? Today, we’re talking about stock dividends, a powerful strategy for building your wealth!

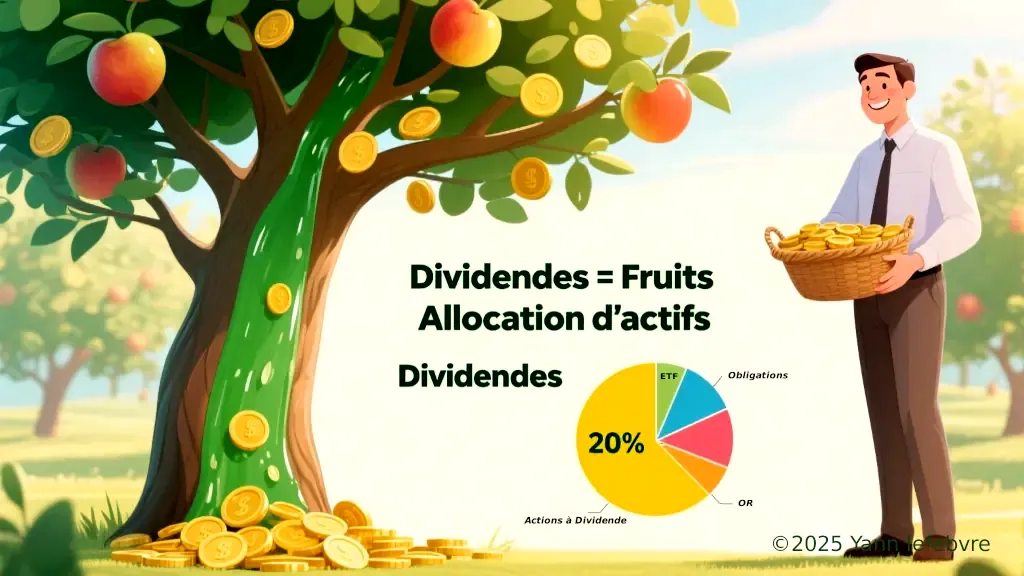

If you’ve watched my video on asset allocation: « How to Optimize Your Asset Allocation in 2025: A Complete Guide for Beginners« , you know that a well-built portfolio relies on a balance between different asset classes: stocks, bonds, real estate, etc.

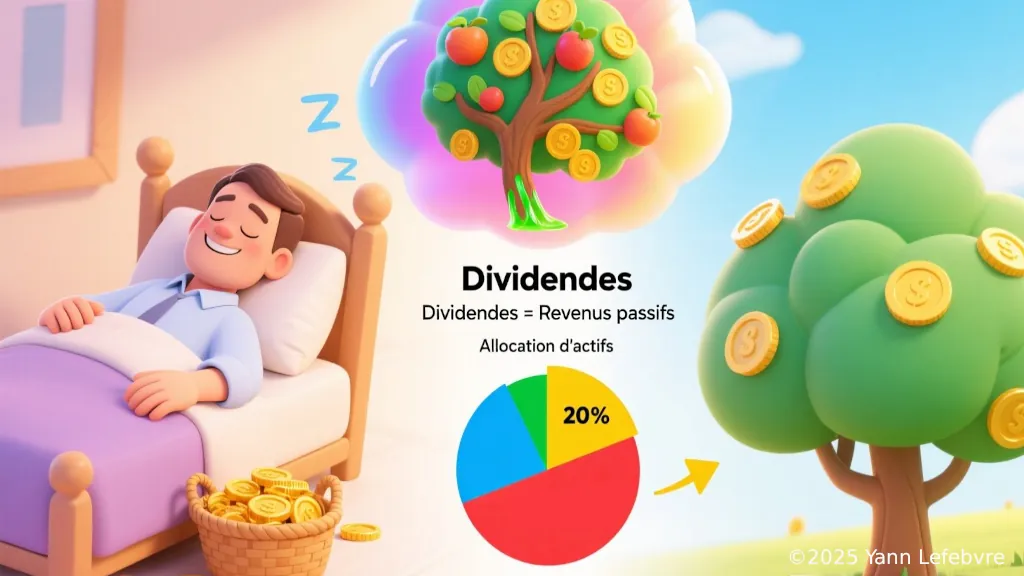

Dividend investing should be integrated into this strategy, depending on your goals and risk tolerance. Dividends—especially through income-focused companies or high-yield stocks—are ideal for those seeking regular income, but they aren’t suitable for everyone. We’ll see how to intelligently incorporate them into your asset allocation.

I’ll define what a dividend is, compare income stocks vs. growth stocks, explain the technical adjustment on the ex-dividend date, and give you tips for choosing the right dividend stocks.

What is a dividend ?

Imagine a company as a fruit tree: every year, this tree produces fruit—dividends—that you, as a shareholder, can pick without damaging the tree. This fruit is a share of the company’s profits, distributed to reward its investors. For beginners, let’s clarify a few essential concepts :

Company profits :

Profit is the net income a company generates after subtracting all its expenses from its revenue. In the metaphor, profit is like the sap or wealth produced by the tree (the company). Part of this sap can be turned into fruit (dividends) distributed to shareholders, while the rest is reinvested to help the tree grow (growth or reserves). This is an internal measure of the company, reflecting its financial health and its ability to generate value.

Example: If TotalEnergies generates €10 billion in revenue and spends €8 billion, its profit is €2 billion. Part of this can be paid out as dividends or gains to shareholders (e.g., €0.74 per share), while the rest is reinvested or kept as reserves.

Financial gain :

Financial gain is the profit an investor makes on an investment, whether through income (such as dividends) or capital gains (the difference between the purchase price and the sale price of an asset). It is specific to the investor, not the company. Financial gain is what you, as a gardener (investor), get by picking the fruit (dividends) or by selling a branch of the tree (capital gains on the sale of shares).

Example: If you buy a TotalEnergies share at €50, receive a €0.74 dividend, and sell it at €60, your financial gain is €0.74 (dividend) + €10 (capital gain) = €10.74 per share.

This is an individual measure, depending on the investor’s choices (buying, selling, holding) and market conditions.

Definition of a dividend :

A dividend is therefore a share of the profits paid out to shareholders, usually in cash, sometimes in additional shares. Example: with 100 shares paying a $2 dividend, you pocket $200 in passive income. Dividends can be paid monthly, quarterly, semi-annually, or annually, and can be regular (predictable) or special (one-off).

Dividend-Paying Companies :

Income companies, such as Coca-Cola or Johnson & Johnson, are like mature trees in stable sectors (consumer goods, healthcare). They pay generous dividends, built into their long-term strategy, because their profits are steady and predictable. Growth companies, like Tesla, reinvest their profits to expand, offering little or no dividends, but with strong capital appreciation potential.

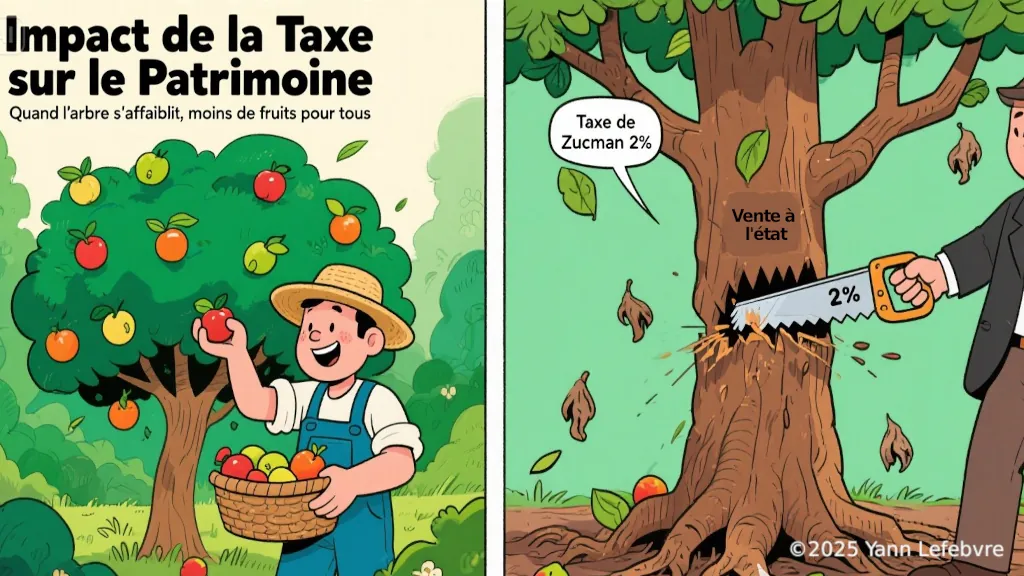

Tax risk (Zucman tax)

In France, a tax like the Zucman tax (2% on wealth, including business shares) could reduce the profits available for dividends. This would force an entrepreneur to sell shares, weakening the company and its future payments, and therefore your financial gains.

In your asset allocation, dividends from income companies provide a stable income, complementing your growth assets. And here’s the good news: the drop in share price on the ex-dividend date is temporary and has no long-term impact, because what really matters is the health of the tree!

Income Companies vs. Growth Companies

Income Companies :

Income companies are like mature fruit trees that produce fruit—dividends—every year. Their strength comes from two things: their maturity, meaning their stability and long track record, like Coca-Cola or TotalEnergies, and their presence in income-generating sectors. These sectors—such as energy (oil, gold mines), finance (banks, insurance), and real estate (property companies like Unibail-Rodamco)—generate steady cash flows thanks to predictable revenue streams, like oil contracts, banking interest, or rental income. This allows them to pay out high and stable dividends, often with yields of 4-8%, and a payout ratio of 50-80% of their earnings.

Growth Companies :

On the other hand, growth companies—like Tesla or Amazon—are young trees that reinvest all their sap—their profits—to grow quickly. They pay little or no dividends, because their goal is to increase the value of the tree (the share price) for financial gains through capital appreciation upon resale.

Dividend Policy :

Income companies have a high payout ratio (50-80%), while growth companies prioritize reinvestment.

The Technical Price Adjustment, the Ex-Dividend Date, and Dividend Policy

Let’s come back to our fruit tree. On the ex-dividend date—the date when the dividend is detached—the tree loses some fruit (the dividend), and the share price mechanically drops by the amount of the dividend. For example, a stock trading at €100 with a €2 dividend will open at €98 on the ex-dividend date. This is a technical adjustment, because the company has distributed part of its value to shareholders.

Why is this drop minimal and often temporary? Within a few hours or days, the share price typically bounces back to its previous level, because the market has already priced in the dividend payment well before the ex-dividend date. Investors anticipate these regular fruits…

In the long term, paying a dividend does not influence the stock price. Why? Because the price depends primarily on the company’s financial health (its earnings, its growth) and market conditions—not on the fact of distributing fruit.

An income company like TotalEnergies, thanks to its maturity and its rent-generating sector (energy), maintains a stable share price over the long term, whether dividends are paid or not. The drop on the ex-dividend date is a one-off event that quickly fades over time, because what really matters is the tree’s ability to keep producing profits.

That said, the dividend policy—that is, the regularity and amount of dividends—can send signals to the market. A stable policy reassures investors and can support the share price. A sudden dividend cut, on the other hand, may signal difficulties and cause the price to drop. But in the long run, these signals are secondary to the fundamentals: earnings, sector, growth prospects.

Why not speculate? Dividends are designed for long-term financial gains, not for playing the share price.

In your asset allocation, choose income companies for their regular passive income, without worrying about temporary drops on the ex-dividend date. In the long run, the stock price depends on the strength of the tree, not on the fruit it bears.

Why Invest in Dividend Stocks?

Dividend stocks, like the fruit of a sturdy tree, offer stable passive income, ideal for strengthening your asset allocation. Income companies—mature and often found in sectors like energy (e.g., ExxonMobil), finance (e.g., JPMorgan Chase), or real estate (e.g., Realty Income)—generate steady profits, enabling reliable dividends. By reinvesting these dividends, you benefit from the snowball effect.

Unlike growth companies (e.g., Tesla), which focus on capital gains upon resale without providing immediate income, income companies prioritize stability. The technical drop in share price on the ex-dividend date is temporary and already priced in by the market, so it has no long-term impact. The goal? To hold these shares over the long term to accumulate passive income, not to speculate on price fluctuations.

How to Choose Dividend Stocks?

Don’t choose a stock solely for its short-term dividend, at the risk of suffering sudden drops if the company is unstable. Prioritize solid companies, capable of producing fruit—dividends—year after year, like a sturdy fruit tree.

Here are the key criteria :

- Yield: Divide the annual dividend by the share price (e.g., €3 dividend on a €100 stock = 3%). Aim for an attractive yet sustainable yield (4-8% for income companies).

- Dividend history: Look for a stable track record, ideally 10 years without a cut—a sign of a well-rooted tree.

- Payout ratio: A ratio of 50-70% of earnings paid out as dividends shows that the company can maintain its payments without weakening itself.

- Financial health: Check earnings, debt, and cash flow, especially in income-generating sectors like energy, finance, or real estate.

For example, well-known non-French companies like Coca-Cola (consumer goods) or Johnson & Johnson (healthcare) offer reliable dividends, with minimal technical adjustments on the ex-dividend date. Their stability ensures long-term passive income, with no significant impact from dividend payments on their share price. In your asset allocation, include these companies to balance the volatility of growth stocks.

Investment Strategies

Build a diversified portfolio according to your asset allocation: include income companies for regular passive income and growth companies for long-term capital appreciation potential. In both cases, prioritize quality companies—ideally financially solid and generating stable profits—preferably international to limit tax risks, such as those related to the Zucman tax.

When we talk about dividends, think regular income, passivity, and compound interest—not short-term trading, ex-dividend dates, or rapid company growth. Some companies sit between these two extremes, combining modest dividends with growth potential. For example, a company like Apple pays a small dividend while remaining growth-oriented. However, your choice should never be based solely on the dividend, but on the company’s financial health—its earnings, stability, and sector (energy, finance, real estate for income stocks). Too many investors are seduced by the allure of quick gains, like a game of chance, when regular, long-term investing—less spectacular—is often more profitable over time.

If choosing dividend stocks feels intimidating, dividend ETFs, such as the Vanguard High Dividend Yield ETF, are an ideal solution. They group together solid income companies, sparing you from worrying about price fluctuations on the ex-dividend date or over the long term. The trade-off? ETF fees, but these remain low for well-managed funds. Check the top holdings of these ETFs to discover high-potential companies and draw inspiration for your own investments.

Macroeconomic risks: the example of the Zucman tax

In France, dividends are already subject to taxation, such as the 30% flat tax. But let’s imagine a more extreme scenario: the Zucman tax, a proposal aimed at taxing 2% of the wealth of the richest individuals, including their stakes in companies.

For an entrepreneur, this means having to pay 2% of the value of their company to the state every year. However, these stakes are often illiquid (no immediate cash available). To pay this tax, they could be forced to sell shares, which would dilute their control, trigger costly restructurings, and hinder investment or innovation.

The result? Negative consequences for the company—loss of competitiveness, even relocations—and for shareholders, with potentially reduced profits and dividends, like a fruit tree producing less fruit. Fortunately, in France, the vitality of economic debates gives hope that policymakers and citizens will be able to limit or adapt such measures to protect entrepreneurship and dividend stability. In your asset allocation, consider diversifying internationally to secure your passive income against these fiscal risks.

Conclusion

In conclusion, beware of the misconceptions circulating on stock market forums, often due to a lack of information. Today, educating yourself is within reach thanks to a revolutionary tool: artificial intelligence. With its ability to synthesize complex data, it helps you deepen your knowledge and invest with confidence.

Dividends, like fruit picked without damaging the tree, fit perfectly into your asset allocation to generate passive income. The drop in share price on the ex-dividend date is purely technical and already priced in by the market, so it has no long-term impact. Whatever the dividend, focus on solid companies—mature and in income-generating sectors like energy, finance, or real estate—for stable income over time. Stay vigilant about fiscal risks, such as the Zucman tax, which could weigh on corporate profits. Fortunately, in France, our economic spirit and common sense will limit measures that hinder entrepreneurship. (LOL)

So, build a resilient portfolio and keep learning! Share in the comments of the upcoming video: how do you integrate dividends into your strategy? And to go further, check out my article on : asset allocation to optimize your investments..

IMPORTANT DISCLAIMER

I am not a financial advisor. I share thoughts that I personally apply and am happy to pass along. This is not investment advice. The views expressed are summarized and mixed with personal reflections that are solely my own. These are ideas to consider; it is essential to educate yourself and seek multiple sources of information to make informed decisions. No buy or sell recommendations are made. Each individual must invest according to their investor profile, risk tolerance, budget, age, personal and family situation, level of financial literacy, and investment horizon. Everyone is responsible for their own financial decisions.